Tag: FinTech

-

How PSD2 is set to shake banking up as we know it …

“Banking is necessary. Banks are not.” Yep. Bill Gates said it. Back in 1994. And 28 years later, it’s it’s set to become reality. From the 1st January 2018, banking will no longer be the exclusive domain of banking institutions because PSD2 is going to drastically alter the way in which we bank. The biggest consequence is that…

-

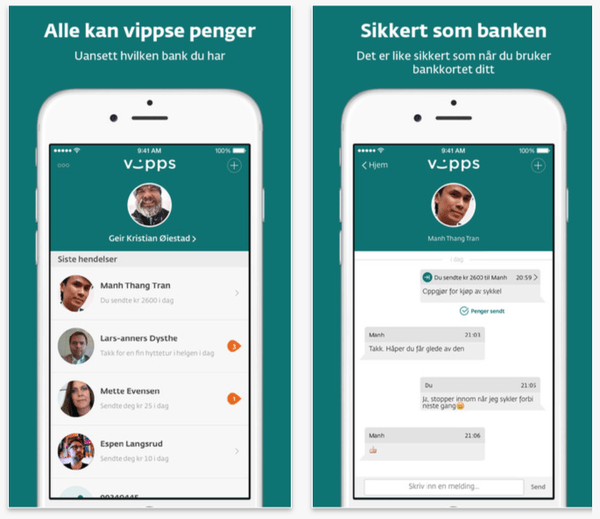

Vipps (Product Review)

I’m always on the lookout for new payment apps and I recently came across Vipps. Vipps is a Norwegian peer to peer payments app, currently only available to Norwegian users. These are the main things I’ve learned about Vipps: Main learning point: Love how apps like Vipps are making it easier and easier for people to pay…

-

THEO (Product Review)

I recently came across THEO, a mobile, Japanese investment service offered by Money Design. THEO acts as a ‘robo-advisor’; enabling users to invest using their smartphone, and applying machine-based learning to offer users investment suggestions. The service allows users to start investment from 100,000 JPY. By answering nine questions (see Fig. 2 below), Money Design’s proprietary robo-advisor’s…

-

Tide (Product Review)

How did Tide come to my attention? – I vaguely recall receiving an email from Tide a while ago about signing up for Tide, and a chance to learn about this new service before launch. My quick summary of Tide (before using it)? – I expect a bank account exclusively geared towards to small to…

-

Learning more about what’s coming under PSD2

The second instalment of Payment Services Directory, “PSD2”, will come into effect on 13th January ’17. By that date, EU member states are expected to have implemented the new payment rules as outlined in PSD2. I recently listened to a radio programme where ex Barclays boss Antony Jenkins described PSD2 as “an opportunity for third parties…