Category: User Experience

-

Lorikeet (Product Review)

My summary of Lorikeet before looking into it – An AI powered customer support agent. How does Lorikeet explain itself in the first minute? “The AI Customer Concierge for complex companies”, which to me suggest that Lorikeet aims to provide a solution to dealing effectively with more complex support queries. Examples such as “flight rescheduled”…

-

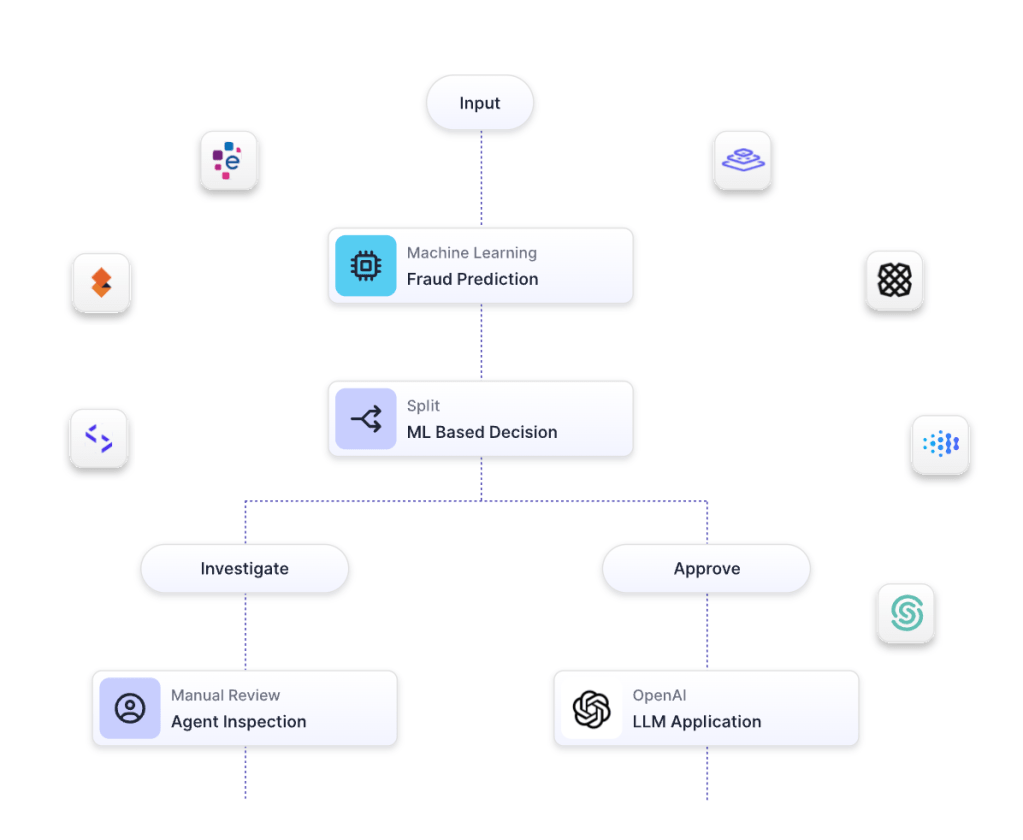

Paperclip (Product Review)

My summary of Paperclip before using it – Before trying Paperclip, I had a rough idea of what to expect: an agentic platform for business tasks, probably something like a smarter to-do list with AI running the items. I was partially right, but the reality is more interesting than that. How does Paperclip explain itself in…

-

How real estate marketplaces are using AI

Real estate marketplaces have a clear commercial incentive to use AI well: the better they match buyers, renters and sellers, the more transactions they facilitate. I started by looking at Property Finder — a marketplace for the Middle East and North Africa (MENA) region, broadly comparable to Rightmove in the UK or Zillow in the…

-

Building a Vibe Coding Assistant in Bolt

I like tinkering with new product ideas. I struggle sometimes with the quality of my prompts – taking my idea and prompting tools like Bolt or Lovable to create a prototype. It’s that classic cold start problem where you don’t know what you don’t know. Just for fun, I wanted to see if I could…

-

Taktile (Product Review)

My summary of Taktile before using it – An automated compliance platform. How does Taktile explain itself in the first minute? When I go to the Taktile website I quickly realise that it’s more than just a compliance platform. Taktile positions itself as “The Decision Platform for the AI Age” and it specialises in intelligent…