Category: AI

-

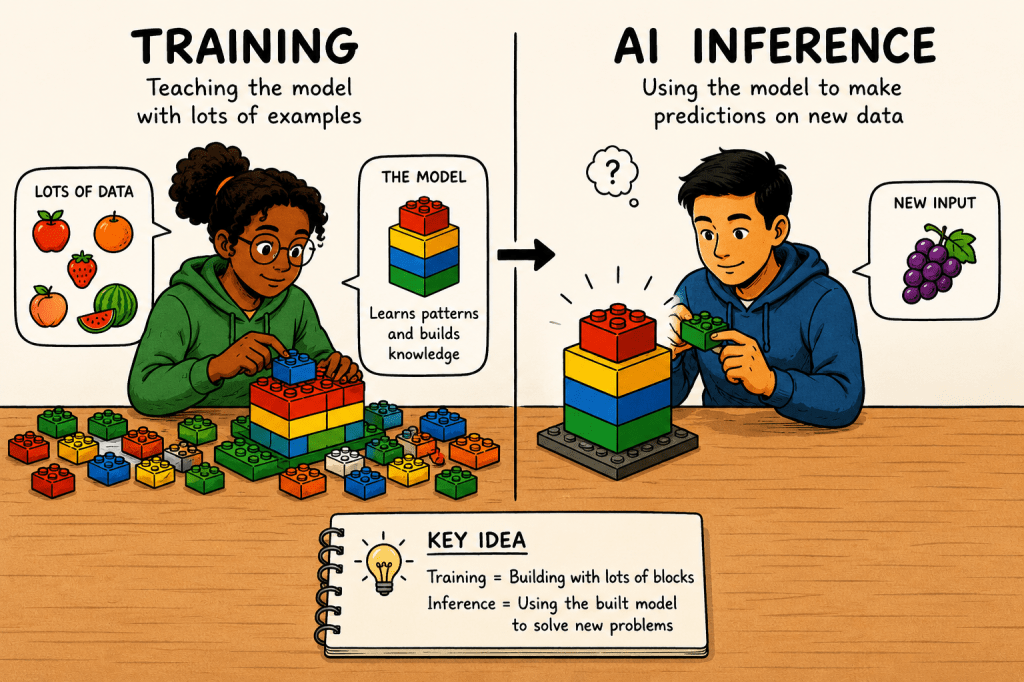

AI inference: what it is and why it matters for product managers

When I first heard the term “inference computing”, I wasn’t entirely sure what it meant. So I looked into it, and the concept turned out to be surprisingly relevant to the way I work with AI tools every day. In simple terms, AI inference is what happens when an AI model that has been trained…

-

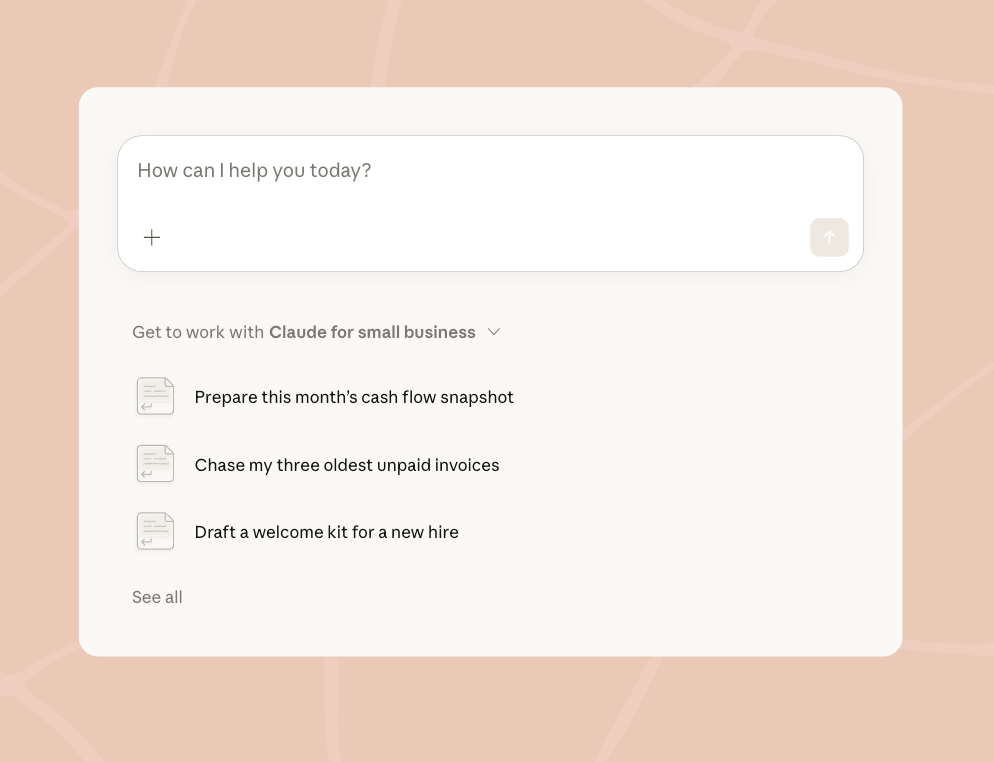

Claude for Small Business (Product Review)

Earlier this year, Anthropic caused ripples across the SaaS world by introducing specific Claude plugins: out-of-the-box workflow solutions spanning legal, marketing, and compliance use cases. It continues to expand in these areas, this time with the launch of Claude for Small Business. Through a dedicated plugin, businesses can now access 15 pre-built workflows to help…

-

Paperclip (Product Review)

My summary of Paperclip before using it – Before trying Paperclip, I had a rough idea of what to expect: an agentic platform for business tasks, probably something like a smarter to-do list with AI running the items. I was partially right, but the reality is more interesting than that. How does Paperclip explain itself in…

-

Adding agentic skills to Claude Code

Over the past couple of months, I’ve been experimenting with skills in Claude Code — and it’s genuinely changed how I work. By creating a SKILL.md file, I can give Claude specific instructions for recurring tasks, getting consistent, high-quality output without repeating myself every session. Skills also follow an open standard, meaning they can work…

-

My Product Management Toolkit (69): AI guardrails

What are AI guardrails? Guardrails identify and remove inappropriate or inaccurate output generated by LLMs. They can also pick up on risky prompts to reduce the risk of leaking sensitive information, sharing personally identifiable information and providing non-compliant advice. Guardrails shape the LLM’s behaviour by setting specific rules that apply to any data input into…