Tag: technology

-

Lorikeet (Product Review)

My summary of Lorikeet before looking into it – An AI powered customer support agent. How does Lorikeet explain itself in the first minute? “The AI Customer Concierge for complex companies”, which to me suggest that Lorikeet aims to provide a solution to dealing effectively with more complex support queries. Examples such as “flight rescheduled”…

-

What is harness engineering?

The more I experiment with AI agents, the more I realise that the model is only part of the story. What sits around the model, the infrastructure that governs how it behaves, what it can do, and when it stops matters just as much. This is what harness engineering is about. An AI harness or…

-

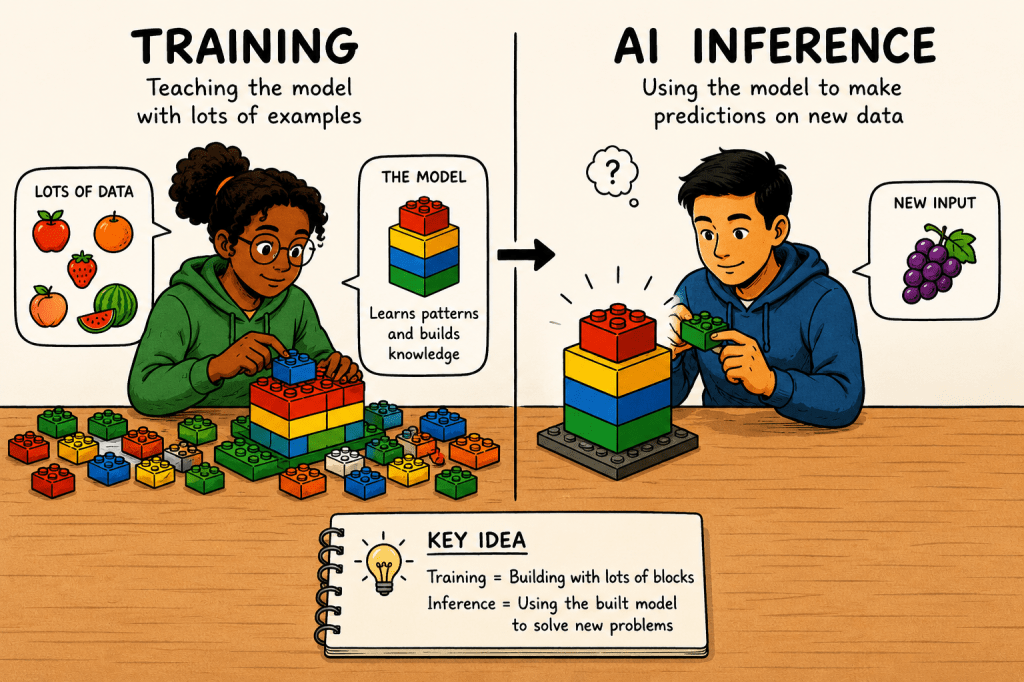

AI inference: what it is and why it matters for product managers

When I first heard the term “inference computing”, I wasn’t entirely sure what it meant. So I looked into it, and the concept turned out to be surprisingly relevant to the way I work with AI tools every day. In simple terms, AI inference is what happens when an AI model that has been trained…

-

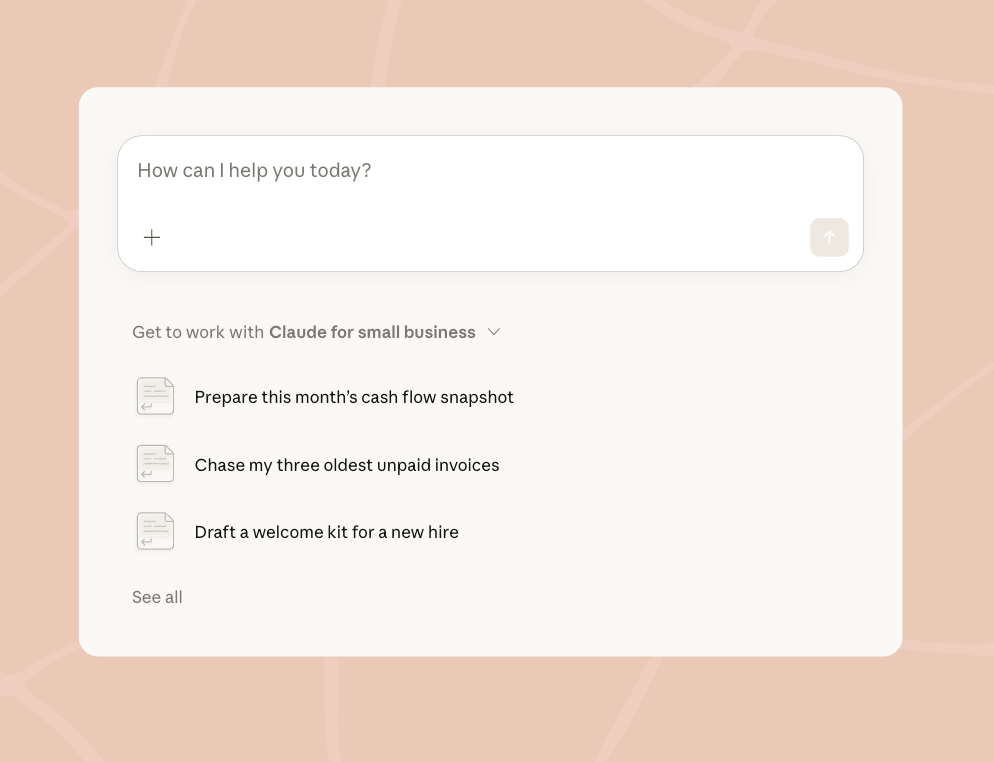

Claude for Small Business (Product Review)

Earlier this year, Anthropic caused ripples across the SaaS world by introducing specific Claude plugins: out-of-the-box workflow solutions spanning legal, marketing, and compliance use cases. It continues to expand in these areas, this time with the launch of Claude for Small Business. Through a dedicated plugin, businesses can now access 15 pre-built workflows to help…

-

Paperclip (Product Review)

My summary of Paperclip before using it – Before trying Paperclip, I had a rough idea of what to expect: an agentic platform for business tasks, probably something like a smarter to-do list with AI running the items. I was partially right, but the reality is more interesting than that. How does Paperclip explain itself in…