“Banking is necessary. Banks are not.” Yep. Bill Gates said it. Back in 1994. And 28 years later, it’s it’s set to become reality. From the 1st January 2018, banking will no longer be the exclusive domain of banking institutions because PSD2 is going to drastically alter the way in which we bank.

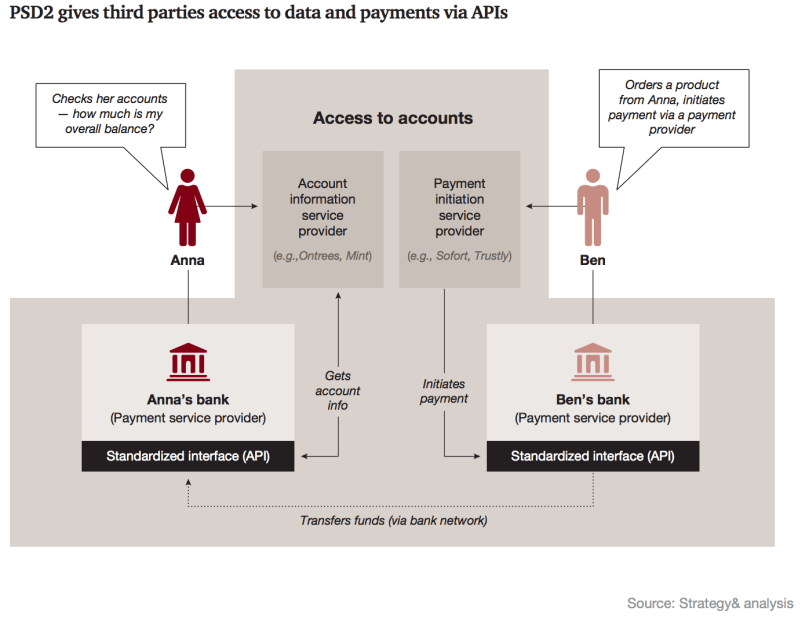

The biggest consequence is that more than 4,000 European banks will need to open their legacy (mainframe) data stores to Third Party Players (‘TPPs’) and allow them to retrieve account information (‘AIS’) or initiate payments (‘PIS’). Both capabilities will be facilitated through APIs. I wrote about the scope and ramifications of PSD2 a few months ago, and I’ve been thinking ever since about the implications for existing banks and whether they’ve got reason to be scared.

It would be surprising if some of the traditional banks weren’t nervous about the extent to which they’ll have to open their kimonos under PSD2. And even if the Facebooks, Googles or Amazons of this world don’t become banks overnight, I expect the traditional, lifelong bank-customer relationship to slowly evaporate as a result of PSD2 (and subsequent versions of PSD).

Facebook could easily decide to become an AISP (Account Information Service Provider – see above), which would enable them to offer an aggregated view of a user’s bank accounts. As a result, they would be able to analyse spending behaviour, understand their users’ financial profiles and personalise a user’s banking experience. This isn’t that revolutionary, as virtual assistants like Cleo and Treefin have already starting offering this functionality, and I believe it’s highly likely that we’ll see it roll out across Facebook Messenger or WeChat in the near future. If you need more convincing, Facebook made their first move two years ago by appointing David Marcus, former CEO of PayPal, to head up Facebook Messenger, so watch this space. Similarly, US bank Capital One integrated with Amazon’s virtual assistant Alexa last year. This integration enables Capital One customers to pay their credit card bills and check their balances, by talking to their Alexa devices.

In addition, any remaining doubters about the power of APIs are likely to be converted as a result of PSD2. In the current Fintech landscape, there already are large number of banks that are either using APIs to hook into existing banking infrastructures (e.g. Varo Money) or offer additional services (e.g. N26). PwC recently conducted a study into the strategic implications of PSD2 for European banks and they listed no less than six API-powered banking business models.

Main learning point: It will be interesting to see what the actual impact of PSD2 will be, but if I were a traditional European bank, I’d be working as hard as I could to open up my APIs from today and start working on the creation of strong alliances with 3rd parties and their developers. As Nas once rapped on “N.Y. State Of Mind”, “I never sleep cause sleep is the cousin of the death.” If I were a traditional bank I’d follow Nas’ advice and give up on sleep completely …

Related links for further learning:

- https://www.finextra.com/blogposting/14101/psd2-is-fast-approaching-dont-bury-your-head-in-the-sand

- https://www.finextra.com/videoarticle/1469/data-is-a-key-legal-issue-for-open-banking

- https://techcrunch.com/2017/01/12/what-facebooks-european-payment-license-could-mean-for-banks/

- http://www.ibtimes.co.uk/apple-facebook-amazon-primed-psd2-demolition-card-networks-1606188

- https://www.siliconrepublic.com/enterprise/fintech-banking-psd2

- http://www.bankingtech.com/675841/psd2-and-the-future-of-payments/

- https://www.evry.com/en/news/articles/psd2-the-directive-that-will-change-banking-as-we-know-it/

- http://www.sepaforcorporates.com/single-euro-payments-area/5-things-need-know-psd2-payment-services-directive/

- https://techcrunch.com/2015/07/12/the-future-of-finance-is-in-real-time/

- https://www.finextra.com/finextra-downloads/newsdocs/catalyst-or-threat.pdf

- http://www.pymnts.com/news/b2b-payments/2015/task-force-launches-eu-instant-payment-plan/.VYpo1rnhBTI

- https://venturebeat.com/2016/06/05/say-hello-to-messenger-banking/

- https://www.finextra.com/newsarticle/28602/capital-one-integrates-with-amazon-alexa-for-voice-powered-payments

2 responses to “How PSD2 is set to shake banking up as we know it …”

[…] become more of a ‘financial hub’ for customers, using APIs and the opportunities that PSD2 offer. I wouldn’t be surprised if ipagoo do more to address cross-border payments, as well as […]

[…] from your mortgage application, , after the boxes have been auto-filled. With the advent of PSD2 and open banking, I expect loads of US mortgage lenders and startups to enable a similar synchronisation with a […]