Category: FinTech

-

ComplyAdvantage (Product Review)

My summary of Comply Advantage before using it – Automated Anti Money Laundering (AML) compliance. Why AML compliance is painful? Having worked with banks previously, I’ve seen first hand the challenges and intricacies of AML – incorporating AML checks into user journeys as well as ongoing risk monitoring. How does ComplyAdvantage explain itself in the…

-

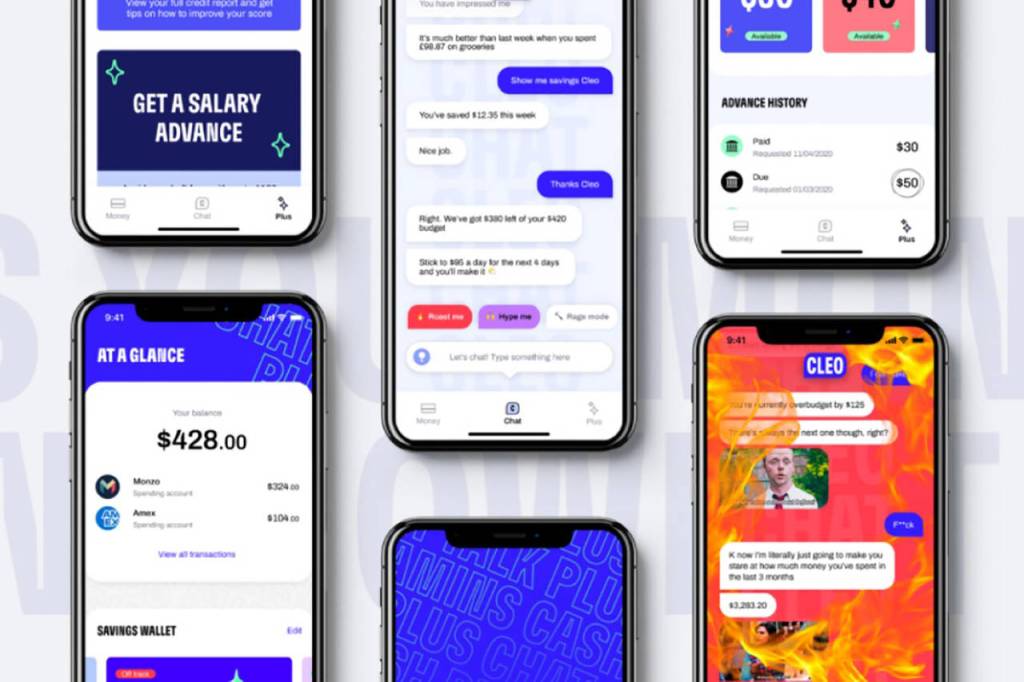

Cleo Financial Assistant (Product Review)

I first reviewed Cleo’s financial assistant a good seven years ago. After rereading my review, I remember Cleo largely meeting my expectations in places; a financial assistant helping users manage and save money. In the last sentence of my review I expressed a desire to “see how Cleo will develop further over the coming months,…

-

Finalytics.ai (Product Review)

My summary of Finalytics.ai before using it – Finalytics is a startup specialising in analytics for banks and other financial institutions. How does Finalytics explain itself in the first minute? “Humanize The Digital Experience” reads the strap-line on the Finalytics website. Through Finalytics, financial institutions can use AI and access a “segment of one digital…

-

Karat (Product Review)

My summary of Karat before using it? I know that Karat is geared towards influencers, people with followings on social media platforms like TikTok and Instagram. I’m probably not part of Karat’s target audience 🙂 How does Karat explain itself in the first minute? “The back card for creators” is the first thing I read…

-

Rocket Mortgage’s Instant Mortgages (Product Review)

Can the whole process of getting a mortgage made a lot easier!? Whether you’re looking to buy a home or refinance your current one, the mortgage process can be a real pain in the neck: slow, stressful and opaque. Given the emergence of players such as Trussle, Habito – both UK-based online mortgage brokers – and my…