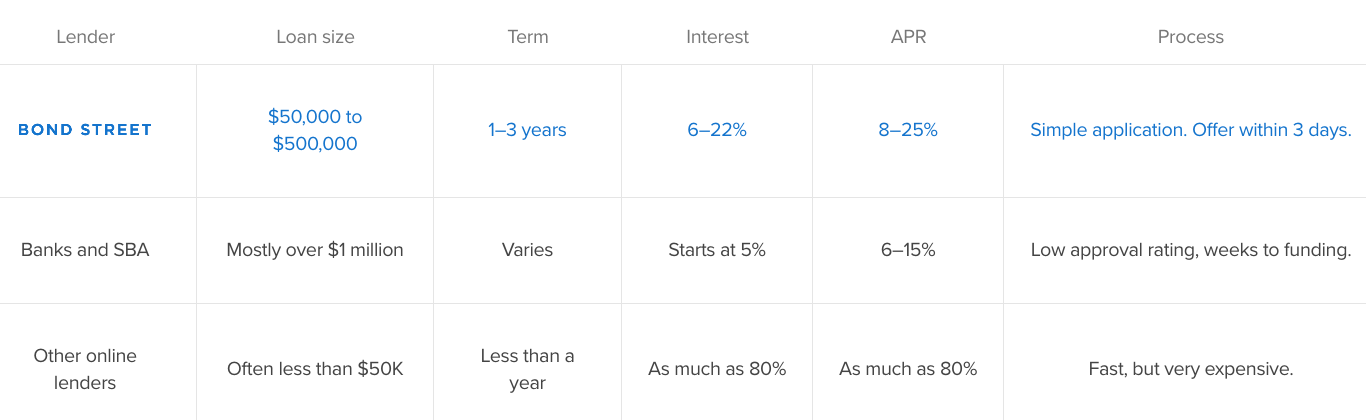

Bond Street lends to small businesses that might typically struggle to get a loan from traditional banks. In a recent talk on a MIT Fintech course that I was doing, David Haber – Bond Street’s CEO/Founder – mentioned how Bond Street saw a clear niche in the market for small business loans and acted on it. Haber encountered a problem that seemed pretty common for early stage, online small businesses: banks or other financial services offering small loans for short durations at high rates. To resolve this problem, Bond Street offers loans range between $50k-$500k, for as long as 1-3 years and with rates starting at 6% (see Fig. 1 below).

Fig. 1 – Loan size, rate and terms comparison between Bond Street and other small business lenders

Fig. 2 – Overview of Bond Street positioning

In the MIT talk, Haber mentioned that OnDeck – a direct competitor of Bond Street – offers small business loans for an average amount of $35k, 10 months’ duration and charges of 40% Annual Percentage Rate (‘APR’). Bond Street competes on rate and speed, but as Haber explained, the business is very focused on “offering more value beyond the economics of a loan, since capital is essentially a commodity.”

Haber then explained that technology allows Bond Street to not just innovate on the loan transaction itself, but to provide a great customer experience on either side of the transaction. For example, by offering a borrower data about similar size businesses, the borrower can then make a better informed decision about taking up a loan.

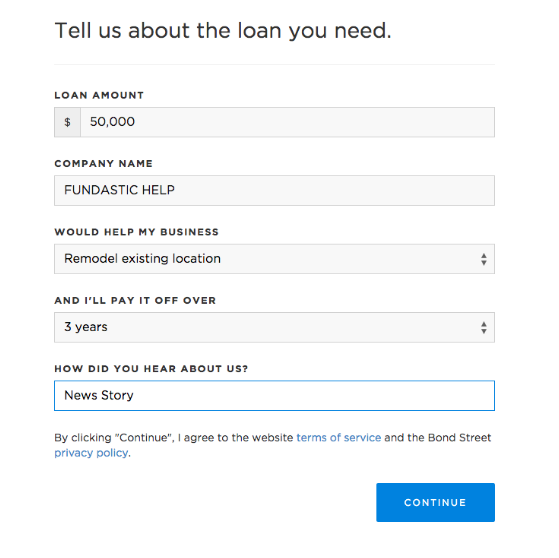

Fig. 3 – Screenshot of Bond Street online loan application form

Haber mentioned one other thing which really resonated with me: “building an ecosystem around your business.” By, for example, leveraging data on an entrepreneur across a network of (similar) entrepreneurs, Bond Street and others can really help people grow their businesses. This doesn’t mean committing data violations, but using data to build an ongoing relationship with one’s customers, and being able to warn them about potential risks or suggest new market opportunities.

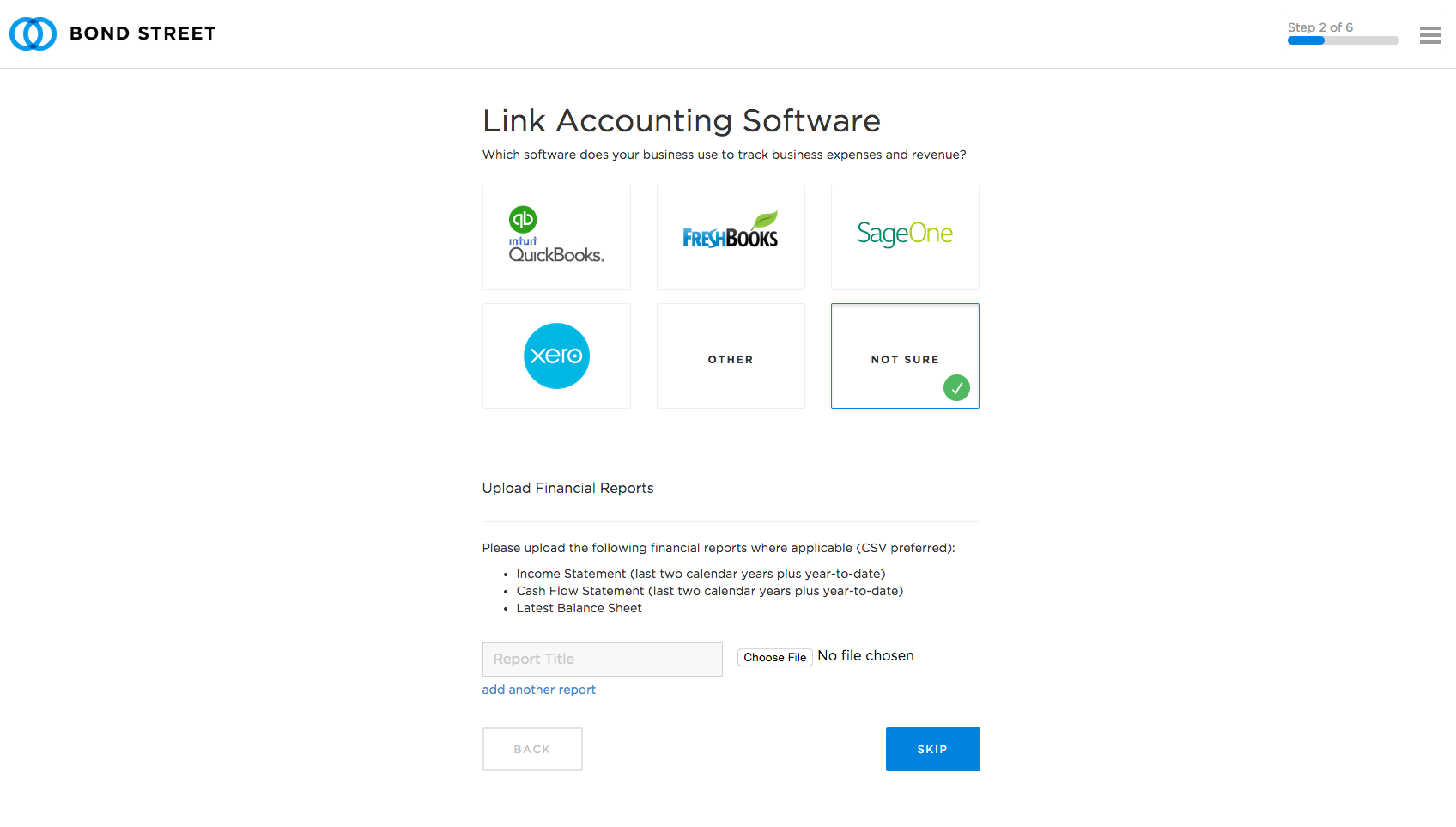

A great example is how easy Bond Street makes it for its customers to link to their accounting packages (see Fig. 4 below). I see this is a simple but good example of creating an ecosystem where data is combined in such a way that people and business can derive tangible benefits from it. Through linking to your accounting package as part of the loan application process, businesses save a lot of precious time and effort, since they no longer have to manually input all kinds of financial data.

Fig. 4 – Screenshot of Bond Street’s functionality which links to one’s accounting software

Main learning point: Even though lending isn’t a new proposition, I really like what Bond Street are doing when it comes to offering loans to small businesses. It has carved out a specific market niche – small, early stage businesses – that it targets with a compelling proposition and an intuitive customer experience to match.

Related links for further learning:

- https://www.thebalance.com/what-does-apr-mean-315004

- https://bondstreet.com/blog/category/resources/

- http://www.forbes.com/sites/laurashin/2015/06/18/6616/

- http://www.peeriq.com/p2p-explosion-business-models-may-change-risks-still-need-managed/

- https://bondstreet.com/blog/an-introduction-to-small-business-financing/

- https://bondstreet.com/blog/a-beginners-guide-to-cloud-based-accounting-software-ii/

- https://www.fundera.com/blog/2016/06/01/application-process-works-bond-street

- https://angel.co/bond-street

- https://www.nav.com/blog/376-decoding-a-loan-offer-from-bondstreet-4788/

- https://www.fundera.com/blog/2016/06/01/application-process-works-bond-street