I recently heard Shamir Karkal, Head of Open APIs at BBVA, talking about open platforms and I was intrigued. In the podcast episode Shamir talked about the power of APIs, but at the same time stressed the importance of having a strong platform that these API end points can hook into.

Shamir talked about building a product with a platform attached. Instead of just building a set of APIs, we should treat APIs as a way in for customers, developers and third parties to hook into the capabilities of our business. For example, hooking into all the things that banks typically tend to do well: compliance, risk management and customer support.

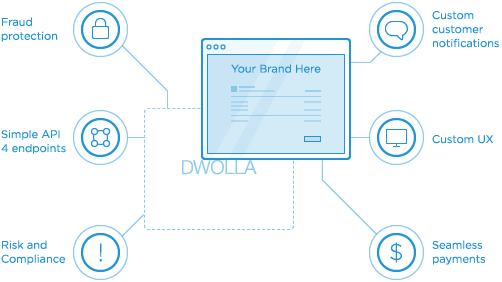

My ears really perked up as soon as Shamir started talking about Dwolla. Dwolla is US based peer-to-peer payments company, whose mission it is to facilitate “Simple payments. No transaction fees.” Dwolla is powered by APIs, making it easy for US users to link their Dwolla account to a US bank account or credit union account to move money. Setting up a Dwolla account is free, and there’s no per transaction fee. Users can collect payment on an invoice, send a one-time or recurring payment, or payout a large number of people at once. Dwolla also offers this a white label solution (see Fig. 1 below).

Fig. 1 – Dwolla’s white label version of their API

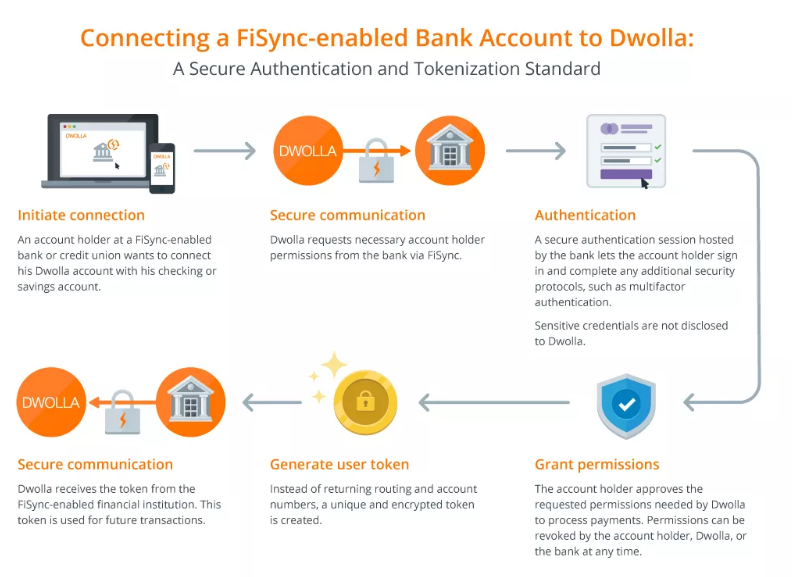

In essence, what Dwolla does is enabling real-time payments between Dwolla accounts and another bank account that users want to send money to. Dwolla are integrated with banks such as BBVA, having Dwolla APIs ‘talk’ to the bank’s APIs. Dwolla has created some form of a protocol in the form of FiSync which aims to make it more secure for users to transmit information between accounts. FiSync enables the use of secure authentication and tokenisation in the comms between Dwolla and accounts like those of BBVA Compass. This way, BBVA Compass account holders don’t have to share their account info with Dwolla (see Fig, 2 below).

Fig. 2 – Workflow of a connecting a FiSync-enabled bank account to Dwolla

Main learning point: I love how Dwolla’s proposition is almost entirely API based, making it easy for its users to transfer money to bank accounts and credit union accounts. Dwolla definitely feels more seamless, secure and cost-efficient compared to the way in which users traditionally transfer money from one account to another.

Related links for further learning:

- http://11fs.co.uk/podcasts/ep111-interviewed-innovators-really-changing-banking/

- https://www.bbva.com/en/news/disciplines/shamir-karkal-building-financial-future-bbvas-platform/

- http://finovate.com/open-api-shamir-karkal-to-head-bbvas-new-developer-platform/

- http://apievangelist.com/2015/09/03/dwolla-just-released-a-white-label-version-of-their-api-are-you-ready-for-the-wholesale-api-economy/

- http://www.ibm.com/support/knowledgecenter/SS9H2Y_7.5.0/com.ibm.dp.doc/oauth_threeleggedflow.html

- https://www.dwolla.com/updates/breaking-down-real-time-secure-authentication/

- http://help.dwolla.com/customer/portal/articles/1940212-bbva-compass-dwolla-faq?b_id=5440

- https://www.bbvacompass.com/compass/dwolla/