It isn’t often that one of the apps that I use on a regular basis attracts a large round of funding but it happened recently with Receipt Bank, a London based started which “makes your bookkeeping, faster, easier and more efficient.” Last month, Receipt Bank received a Series B investment worth $50 million from New York based Insight Venture Partners.

Receipt Bank, which started in 2010, targets accountants, bookkeepers and small businesses. It offers them an online platform through which users can submit their invoices, receipts, and bills by taking a picture and uploading it through Receipt Bank’s mobile app (see Fig. 1), desktop app (see Fig. 2), or an email submission. Receipt Bank’s system then automatically extracts relevant data, sorts and categorises it. Apart from viewing your processed expenses online, Receipt Bank also publishes everything to the user’s accounting software of choice, FreshBooks or Xero for example.

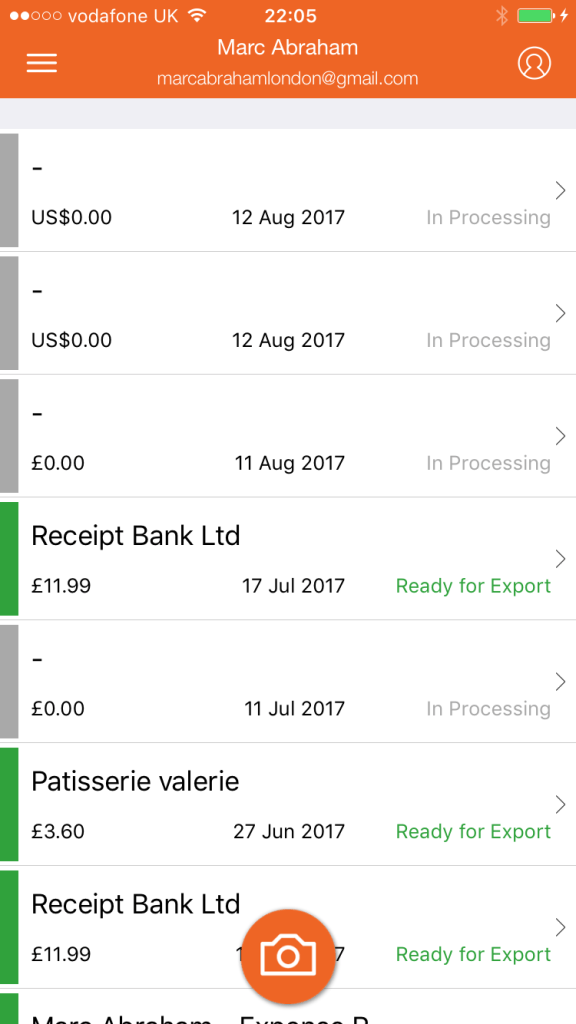

Fig. 1 – Screenshot of Receipt Bank iOS app:

Fig. 2 – The entry in Receipt Bank for one of my receipts:

Given that I’ve been using Receipt Bank for a while now; instead of just reviewing existing functionality, I’ve also had a think about how I’d use a $50m war chest to further build out the Receipt Bank product:

- Faster! Faster! Faster! – When I started using Receipt Bank last year, I emailed the customer support team enquiring about the wait between submitting a picture of a receipt and it being “ready for export”. I got a friendly reply explaining that “we ask for a maximum of 24 hours to process items, but we are usually much faster than that.” The customer support adviser also explained that “the turnaround time also depends on the number of items waiting to be processed by the software and also their quality.” I’m sure Receipt Bank uses some form of machine-learning, algorithms to automatically interpret and categorise the key data fields from the picture of a receipt. As the field of Artificial Intelligence continues to evolve, I expect Receipt Bank to be able to – eventually – process receipts and invoices within seconds, with no need for the user to add or edit any info processed. Because I envisage machine learning to be the core driver of Receipt Bank’s proposition, I suggest spending at least half of its latest investment on AI technology and engineers specialised in machine learning.

- Not just tracking my bills and invoices – Yes, everybody is jumping on the chatbot wagon (and some of the results are frankly laughable). However, I do believe that if Receipt Bank can learn a sufficient amount about its customers and their spending and accounting behaviours, it will be able to provide them with tailored advice and predictions. For example, if I pay my supplier in China a fixed amount per month to keep my stock up, I’d like to ask Receipt Bank’s future “Expense Assistant” how my supplier payments will be affected if there’s massive volatility in the exchange rate between the British Pound and the Chinese Yuan. Similarly, when I look at most of today’s finance departments, the people in these teams seem to spend on matching the right payments received to the relevant invoice(s) sent out. I realise that the machine learning around multiple invoices wrapped into a single payment is easier said than done, but I don’t think it will be impossible and the $25m investment into AI (see point 1. above) should help massively.

- What if the days of paper bills are numbered!? – Now that I’ve effectively spent $25m on AI technology, I’ve got $25m left. The first thing I’d do with this remaining money is to prepare for scenarios where invoices or receipts are no longer issued on paper but provided orally. At the moment, capability like Alexa Expense Tracker is mostly used for personal expenses, but I do envisage a future where people use Alexa or Siri to add and track their expenses. Given that voice technology is still very much in its infancy, I suggest restricting Receipt Bank’s investment into this area to a no more than $1m.

- Integrate more (and please don’t forget about Asia) – If I were Receipt Bank I’d probably use about $10m of the remaining fund to enter new geographies and integrate with additional systems. For example, I like how Sage’s Pegg hooks into any expenses you record on your mobile, whether it’s via Slack, Facebook, Skype, WhatsApp, etc. I don’t know whether Receipt Bank is looking to enter the Asian market, but I feel there’s great opportunity to integrate with messenger apps like WeChat and Hike, without spending more than $2m on development and marketing. Also, integrating with payment processors, like Finsync did recently with Worldpay, is an integration avenue worth considering!

- But don’t forget about the current product! – I feel Receipt bank would be remiss if it were to forget about improving its current platform, both in terms of functionality and user experience. For example, I can’t judge how well Receipt Bank does in retaining its customers, but I feel there are a number of ways in which it can make the existing product ‘work harder’ (see Fig. 3 below). In my experience, some of my proposed improvements and features shouldn’t break the bank. By spending about $1m on continuous improvements over a number of years, Receipt Bank should have at least $20m left in the bank, as a buffer for difficult times and any new opportunities that might arise during the product lifecycle.

Fig. 3 – Suggestions to make Receipt Bank’s existing product work harder:

- Some touches of gamification – I’d argue that the longevity of the relationship between Receipt Bank and an individual user is determined by how often the users uploads bills onto the platform. I assume that most users will most probably not view managing their expenses as fun, I think it would be good to look at ways to make the experience more fun. For example, I could get a gold star from my accountant once I’ve successfully synced my month’s expenses into my accounting system. I feel that there’s plenty of room to reinforce the current gamification elements that Receipt Bank uses. For example, the message that Receipt Bank managed to save 27 minutes of my time doesn’t really do it for me (see Fig. 4 below). Instead, the focus could be on the productivity gain that I’ve made for billable work (if I’m a freelancer for example).

- Better progress and status updates – Even if it does continue to take up to 24 hours. to categorise and process my expenses, it would be great if Receipt Bank could make its “in progress” status more intuitive and informative.

- Clearer and stronger calls to action – For example, I can see that I’m not making the best use of my Receipt Bank subscription (see Fig. 5 below). However, there are no suggestions on specific actions I can take to get more value from my Receipt Bank plan.

Fig. 4 – Screenshot my Receipt Bank usage

Fig. 5 – Screenshot of my Receipt Bank “Usage summary”

Main learning point: Having thought about Receipt Bank’s current product offering, and my understanding of their target market, I suggest investing a good chunk of the recent investment into optimising the machine learning algorithms in such a way that both processing speed and accuracy are significantly increased. By doing this, the customer profile and behavioural data generated, will create additional opportunities to further retain customers and offer adjacent products and services.

Related links for further learning:

- http://uk.businessinsider.com/receipt-bank-raises-50-million-from-insight-venture-partners-2017-7

- https://venturebeat.com/2017/07/20/receipt-bank-raises-50-million-insight-venture-partners/

- https://itunes.apple.com/gb/app/receipt-bank-business-expense-scanner-tracker/id418327708?mt=8

- https://play.google.com/store/apps/details?id=com.receiptbank.android&hl=en_GB

- https://www.forbes.com/sites/bernardmarr/2017/07/07/machine-learning-artificial-intelligence-and-the-future-of-accounting/#49bb42ac2dd1

- https://hellopegg.io/

- http://uk.pcmag.com/cloud-services/87846/feature/23-must-have-alexa-skills-for-your-small-business

- https://www.accountingweb.co.uk/tech/accounting-software/case-study-receipt-banks-rapid-growth

- https://www.finextra.com/pressarticle/70263/finsync-connects-with-worldpay-us

- http://www.bankingtech.com/520502/symitars-episys-core-system-integrated-with-amazon-echo-baxter-cu-an-early-taker/

3 responses to “Receipt Bank (Product Review)”

[…] where you can find applications for things like processing meal receipts (which reminded me of Receiptbank) and identity […]

[…] where you can find applications for things like processing meal receipts (which reminded me of Receiptbank) and identity […]

[…] you will discover purposes for issues like processing meal receipts (which jogged my memory of Receiptbank) and identity […]