I recently had to think back to the words of a well-known London-based Fintech CTO who talked about how in Asia, the Fintech playing field is miles ahead compared to some of the things that are happening in Europe and in the US. His comments came to mind when I overheard a conversation between two, ‘more traditional’ shall we say, senior financial service people, talking about “definitely worth having a mobile app, since that’s what people want and expect.”

To be clear, I’m not trying to knock apps, especially if you look at the amazing apps that the likes of Revolut, Simple and Monzo have created. However, I can’t help try to look ahead and figure out what could be around the corner. For example, I recently looked at PayKey, which integrates payments with messenger apps. The likes of KakaoTalk and Line are already doing this successfully.

I do feel though that all these products are simple dwarfed by the scale with which WeChatPay and Alipay have been adopted, predominantly in Asia:

WePay by Tencent (Tencent is known as Weixin in China)

Even though the functionality of the continental version of WeChat feels quite limited, it’s easy to see how WeChat has evolved rapidly from just a messenger app to platform which incorporates gaming, shopping and payments. WeChatPay, the payment functionality built into WeChat, enables peer-to-peer money transfers, make payments online and with participating offline retailers.

Fig. 1 – Screenshot of WeChat payment interface – Taken from Walkthechat

There are a number of different types of WeChat payment applications:

- App Payment – For Android / iOS apps wanting to include WeChat as a payment option

- Offline Payment – WeChat Offline Payment is meant for brick-and-mortar stores wanting to add WeChat payment via QR codes

- Official Account Payment – This application is used in order to embed WeChat payment within a mobile website

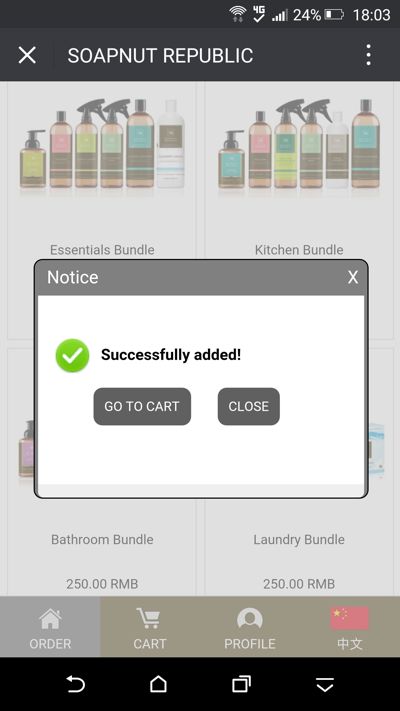

By integrating with WeChat messaging and payment functionality, brands are creating a very seamless user experience and are interacting where their (target) customers already are. Soapnut Republic and its integration with WeChat’s payment functionality is a good example (see Fig. 2 below).

Fig. 2 – WePay screenshot, once a user has completed shopping, she can either use her card to pay or use WeChat’s mobile wallet – Taken from Clickz.com

JD.com – a big Chinese ecommerce platform – has got redirects with WeChat. For example, when customers following the Moleskine account on WeChat want to make a purchase, they are redirected (within the WeChat app) to the brand’s mobile-friendly store on JD.com (see Fig. 3 below).

Fig. 3 – WePay screenshot, once a user has completed shopping, she can either use her card to pay or use WeChat’s mobile wallet – Taken from Clickz

I can imagine that when WeChat launches its new “mini-apps” service in a few days time, its market presence will increase even more. These mini-apps are a type of app that one can use immediately, without having to download or install anything. Users scan a QR code or search and can immediately open an app.

Fig. 4 – Example of WeChat mini-app – Taken from Walkthechat

As WeChat has only launched a developer Beta version of its new mini-apps, I haven’t yet had a chance to play with the apps. However, I’ve learned that through mini-apps users and businesses will most probably be able to (1) do voice recording (through the WeChat API) (2) login (the app will also enable voice recognition) (3) send messages to users and (4) build web apps and services on top of the app.

One will be able to access mini-apps through a special panel, which will be accessible from the “Discover” section of a user’s WeChat account. These mini-apps enable storage of some of the data and code directly on one’s phone, which no doubt will help with app performance and speed.

Alipay by Ant Financial

Forget about traditional banks, Alipay’s ascension and reach has been incredible. Its parent company Ant Financial is controlled by Jack Ma, the founder of ecommerce platform Alibaba. This gives Ant Financial access to all of Alibaba’s ecommerce businesses and the merchants who sell through the platform. Through ownership of Alipay, Ant Financial plays a part in about 65 per cent of China’s online payments and about 80 per cent in the mobile space.

Fig. 5 – Screenshot of Alipay’s mobile wallet – Taken from TechinAsia

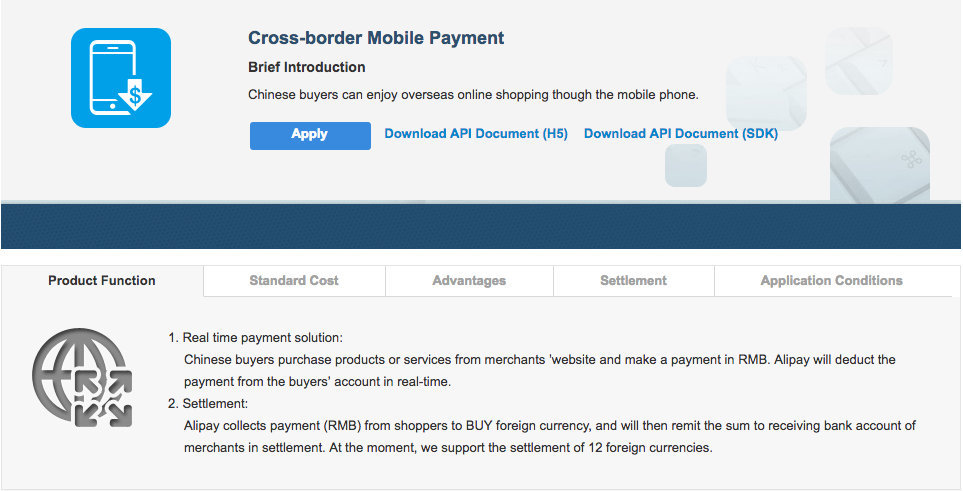

Given the role that Alipay plays in the ecosystem of online buyers and sellers, it’s interesting to look at how Alipay facilitates cross-border mobile payments and how it supports settlement with overseas merchants in 12 foreign currencies (see Fig. 6 below).

Fig. 6 – Alipay’s cross-border mobile payment capability – Taken from: https://global.alipay.com/product/mobilepayments.htm

Until writing this piece, I hadn’t realised that Ant Financial has a stake in Paytm, which is claimed to be India’s largest mobile and ecommerce platform (see Fig. 7 below).

Fig. 7 – Screenshot of Paytm’s iOS mobile wallet

Main learning point: Call me a clairvoyant, but I can see how the likes of Alipay and WeChat will soon take over the world – from a payments perspective at least – purely because of the scale at which they operate and the way they’re nested in a large, diverse ecosystem of online services and users.

Related links for further learning:

- https://intheblack.com/articles/2016/07/01/alipay-and-wechat-are-making-china-a-global-payments-power

- https://news.ycombinator.com/item?id=11347387

- http://en.people.cn/n3/2016/0902/c98649-9109330.html

- http://www.fintechasia.net/alipay-vs-wechat-war-of-chinese-payments/

- https://walkthechat.com/wechat-payment-5-reasons-tencent-might-kill-alipay/

- http://www.beyondsummits.com/blog/alipay-vs-wechat-how-does-alipay-overturn-world-through-scenario-based-payment

- http://www.wsj.com/articles/china-mobile-payment-battle-becomes-a-free-for-all-1463945404

- http://a16z.com/2015/08/06/wechat-china-mobile-first/

- https://www.techinasia.com/kakaotalk-kakaopay-mobile-epayments-korea

- https://techcrunch.com/2016/11/16/tencent-q3-2016/

- https://techcrunch.com/2016/03/17/messaging-app-wechat-is-becoming-a-mobile-payment-giant-in-china/

- https://techcrunch.com/2016/03/08/alibabas-ant-financial-raising-new-funding-at-60b-valuation-ahead-of-ipo/

- https://www.techinasia.com/day-with-wechat-payments-in-stores

- https://intheblack.com/articles/2015/12/01/how-wechat-is-reshaping-facebooks-social-media-future

- https://walkthechat.com/wechat-payment-5-reasons-tencent-might-kill-alipay/

- https://www.clickz.com/how-coach-and-moleskine-use-wechat-for-ecommerce/100300/

- https://curiositychina.com/blog/archives/3095

- https://stripe.com/docs/alipay

- https://global.alipay.com/product/mobilepayments.htm

- http://blog.grata.co/new-wechat-mini-apps/

- https://walkthechat.com/wechat-mini-apps-look-like/

4 responses to “How Alipay and WeChat are setting the tone for payments”

[…] Fintech activity in seven vertical markets – EY/DBS’ report outlines the seven key verticals in which Chinese Fintech businesses are active (see Fig. 1 below). At a first glance, that the lion’s share of innovation by Chinese Fintech players thus far has been in the payments and e-wallets space. I’ve written previously about the absolute rise of alternative payment methods in China, mostly via mobile and predominantly driven by Alipay and WeChat. […]

[…] party integrations – Toutiao has got strategic partnerships in place with the likes of WeChat, a highly popular messaging app, and jd.com, a local online marketplace. It’s easy to see […]

[…] with the aforementioned Meituan company, and Tujia, a Chinese version of Airbnb. Lee also mentions WeChat and Alipay, describing how both companies completely overturned China’s all-cash economy. More recently, […]

[…] to buy or join an existing team. This all happens on relevant social media platforms, mostly on WeChat which is China’s most popular messaging app. The network effect thus created around a product […]