In a few weeks’ time, I’ll be travelling to Hong Kong for the first time, looking to visit Shenzhen as well. I’m hoping it will be a great opportunity for me to learn more about the needs of Chinese customers and get a better feel for the Chinese Fintech scene. To start preparing for my trip, I used a recent report by EY/DBS Bank titled “The Rise of FinTech in China” to learn more about key characteristics of the Chinese Fintech space.

I’ve looked at the ‘current state’ of Fintech in China, both from a customer and a market perspective, and these are my main takeaways from the EY/DBS report:

- Fintech activity in seven vertical markets – EY/DBS’ report outlines the seven key verticals in which Chinese Fintech businesses are active (see Fig. 1 below). At a first glance, that the lion’s share of innovation by Chinese Fintech players thus far has been in the payments and e-wallets space. I’ve written previously about the absolute rise of alternative payment methods in China, mostly via mobile and predominantly driven by Alipay and WeChat.

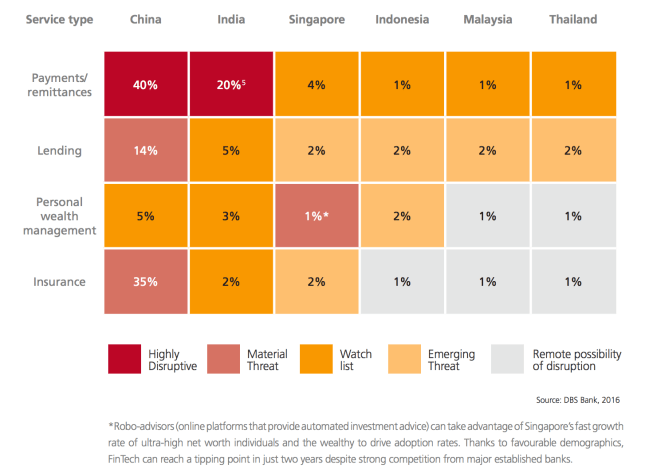

- Chinese customers are embracing alternative payment and insurance methods – The EY/DBS report contains a useful diagram that outlines the percentage of customers per Asian country using specific Fintech services (see Fig. 2 below). Based on this diagram, it looks like both payments/remittances and insurance are already quite established in China, with opportunities for lending and personal wealth management to truly take off soon.

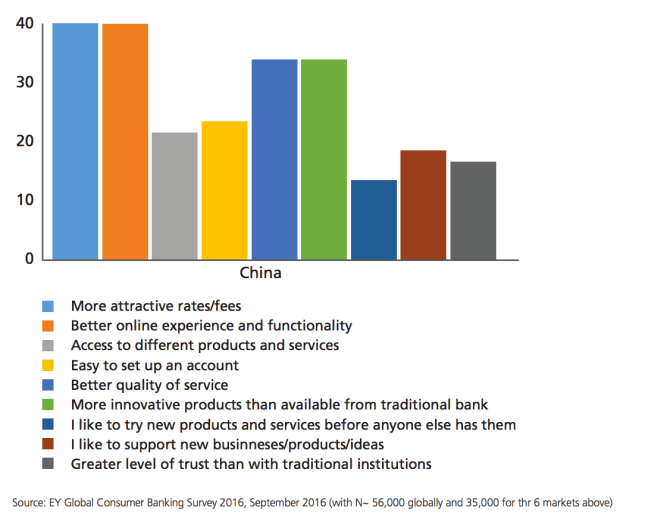

- Customer focus on online experience and functionality – A recent study by EY explored the appetite of Chinese consumers for non banks over traditional banks. It was interesting to read about the value placed on “better online experience and functionality”, as a key reason for using non banks over traditional players. One of my assumptions here is that Chinese consumer prefer banking services which are fully integrated into their daily lives, thinking about how WeChat seamlessly integrates payments into its messenger app.

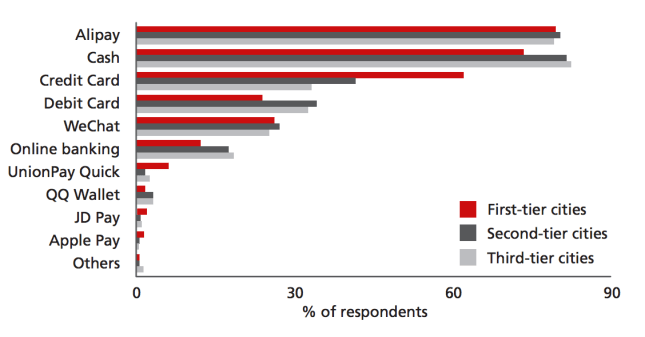

- Alternative payment methods; disruption hasn’t finished yet – I had never given that much thought to low credit card penetration rates across China, but the stats in the EY/DBS report speak volumes in this regard (see Fig. 4 below). The report offers a pretty straightforward explanation for this phenomenon; a strong adoption of alternative payment methods and e-wallets. Unionpay Quick is a good example of a contactless payment method that is becoming more and more ubiquitous in China, particularly in so-called “first tier cities”.

Main learning point: Having read the EY/DBS report, I do feel that China is quite far ahead of the Western world in certain areas of Fintech, particularly in the payments and e-wallet space. In the west, Fintech has been responsible for a lot of ‘unbundling’ of traditional banking services. In Asia – in China in particular – my feeling is that things are moving in the opposite direction: seamlessly integrating financial activities with people’s day to day activities. Alipay, WeChat and, in India, Paytm are leading the way in this regard.

Fig. 1 – Chinese FinTech activity in seven key vertical markets – Taken from: “The Rise of FinTech in Asia – Redefining Financial Services” by EY / DBS

- Payments and e-wallets A mobile payments ecosystem facilitated by e-commerce and social media players, of which Alipay (of Ant Financial) and Tenpay (a Tencent company) dominate the market. Other notable players include UnionPay, ICBC e-wallet, JD Pay/Wallet (of JD.com) and 99bill (of Dalian Wanda Group).

- Supply chain and consumer finance E-commerce players lend to underbanked or unbanked individuals and small medium enterprises (SMEs) by leveraging users’ merchant data on the platform. Key participants include Ant Financial and MyBank (Alibaba), WeBank with WeChat (Tencent), JD Finance (JD.com) and Gome Electronic Appliance, which recently ventured into providing financial services for individual customers and suppliers.

- Peer-to-peer (P2P) lending platforms P2P platforms create a marketplace for peers to lend to individuals and SMEs underserved by the traditional lending sector. Market leaders are Lufax (Ping An Insurance), Yirendai (CreditEase), Rendai, Zhai Cai Bao (Alibaba) and Dianrong (the co-founder of Lending Club).

- Online funds Funds linked to payment platforms that offer ease of access and more competitive returns than the historically low deposit rates. Primary participants are Yu’e Bao of Ant Financial, Li Cai Tong (Tencent) and Baifa (Baidu).

- Online insurance E-insurance sold through e-commerce and online wealth management (WM) platforms. Notable brands are platforms by the People’s Insurance Company of China (PICC), Ping An, and Zhong An (in partnership with Ping An).

- Personal finance management Recently developed mobile-centric finance solutions providing access to mutual funds though stock trading apps. These platforms offer offline-to-online activity, with online brokers accounting for over 92% of new clients. Key players include Ant Financial (Alibaba), Li Cai Tong (Tencent), Baifa (Baidu), Wacai, Tongbanjie, Zhiwanglicai (CreditEase) and JD Finance (JD.com).

- Online brokerage Investment, social network and information portals for investors in China, providing thematic investing via websites and mobile apps, and offered by FinTech firms such as Snowball Finance, Xianrenzhang and Yiqiniu.

Fig. 2 – Percentage of banking/financial services customers using FinTech services – Taken from: DBS Bank, 2016

Fig. 3 – Reasons for using a non-bank rather than traditional bank – Taken from: EY Global Consumer Banking Survey 2016

Fig. 4 – Payment method used most regularly the past 3 months – Taken from: FT Confidential Research survey, May 2016